Casino not on GAMSTOP: what to check before you risk money or personal data

The phrase can sound simple, but it sits at the meeting point of self-exclusion, licensing, payments, identity checks and personal control. This guide explains the practical checks that matter before you act, without naming operators or treating protective systems as obstacles.

A careful decision starts with the boring details: who runs the site, what rules apply, how money moves and what protections are already in place.

Loading...

The plain answer

A casino described as “not on GAMSTOP” is not automatically safer, more private, easier to withdraw from or lawful for a UK user. The phrase only tells you that the site may not participate in the GAMSTOP online self-exclusion system. It does not replace licence checks, terms checks, payment checks, identity checks, complaint checks or a serious look at whether gambling is a good idea for you right now.

GAMSTOP is a free online self-exclusion tool available to people living in the UK. The verified wording for this guide says it applies to online gambling companies licensed in Great Britain, and that an exclusion cannot be removed during the minimum exclusion period. That boundary matters. If you are already excluded, searching for a site outside the scheme can be a warning sign rather than a shopping task.

People usually arrive at this topic for one of several reasons. Some are confused because they have seen the phrase on comparison pages or forum posts. Some want to know whether a site is real before sending money. Some are worried about blocked payments, document requests, delayed withdrawals or bonus terms. Some are self-excluded and feel pulled toward gambling anyway. These are different situations, and they need different answers.

This guide keeps those situations separate. It does not list gambling sites, rank offers, invent bonuses or suggest ways to get around a self-exclusion or a bank block. Instead, it gives you a practical framework: understand the phrase, check who you are dealing with, read the money terms before paying, respect protective tools and know when the safer next step is to stop.

Key takeaway

“Not on GAMSTOP” is not a trust mark. Treat it as a prompt to slow down. If a site relies on that phrase as its main attraction, you still need to ask who licenses it, which domain is covered, what happens to your money, how withdrawals work, what documents can be requested and whether using the site would undermine a protection you already chose.

At a glance: which question are you really trying to answer?

The safest answer depends on the real problem behind the search. A person trying to understand GAMSTOP needs a different explanation from someone who has a delayed withdrawal, a rejected card payment or a worry about identity documents. Use this table to choose the right next step without turning everything into one vague answer.

Reader questions and the safest route through the guide

Your question

Safe first answer

Focused page

What does “not on GAMSTOP” actually mean?

It points to a self-exclusion boundary, not to safety, legality or quality.

Understand the GAMSTOP boundary

How do I know whether a gambling site is accountable?

Check the official public register, the exact domain, business details, restrictions and complaint route before paying.

Check a site before sending money

Why is a site asking for identity documents or delaying withdrawal?

Age and identity checks can be part of gambling controls, but terms, timing and withdrawal rules still need close reading.

KYC, bonuses and withdrawals

Why did a payment fail, or what do bank blocks mean?

Credit-card gambling payments are restricted in Great Britain, and bank blocks can be protective controls.

Payments and bank controls

I am excluded or trying to control gambling. What should come first?

Protection comes before comparison. GAMSTOP, bank blocks, blocking software and support can work together.

Support and protection tools

What if there is a dispute, customer-fund concern or data worry?

Look for the complaints process, ADR route, fund-protection disclosure and data rights information.

Complaints, funds and personal data

Why the phrase can mislead

The wording “casino not on GAMSTOP” often makes a technical boundary sound like a product category. That is the first risk. The phrase does not tell you whether a site is licensed for your location, whether the domain is covered by any licence, whether the operator has a clear complaint route, whether customer funds have a declared level of protection, whether bonuses are understandable, or whether withdrawals will be smooth.

A second risk is emotional. If you have used self-exclusion, card controls or bank blocks, the phrase may appear at the exact moment when a protective pause is trying to do its job. A calm guide should not turn that moment into a sales pitch. It should help you recognise the difference between curiosity, due diligence and the urge to undo a boundary that was put in place for a reason.

A third risk is that overseas licensing, mirror domains and payment routes can be difficult to understand. You should not have to guess from a badge in a footer or a promise on a promotional page. The safer approach is to work from official checks and from the terms that govern your money and personal information.

Phrase, safer interpretation and what not to assume

“Not on GAMSTOP”

May mean the site is not part of the GAMSTOP online self-exclusion scheme.

Do not assume it is trustworthy, suitable or lawful for you.

“Easy withdrawals”

Should be checked against terms, identity rules, bonus conditions and complaint options.

Do not assume a promise means your withdrawal will be paid without checks.

“No hassle verification”

Identity and age checks may still apply, and document requests can vary.

Do not send documents if you cannot verify who receives them and why.

“Alternative payments”

Payment availability does not answer whether the operator is accountable.

Do not treat a working deposit route as a safety check.

Keep the decision in separate boxes: self-exclusion, licensing, payment route, identity checks, complaint path and personal control are not the same question.

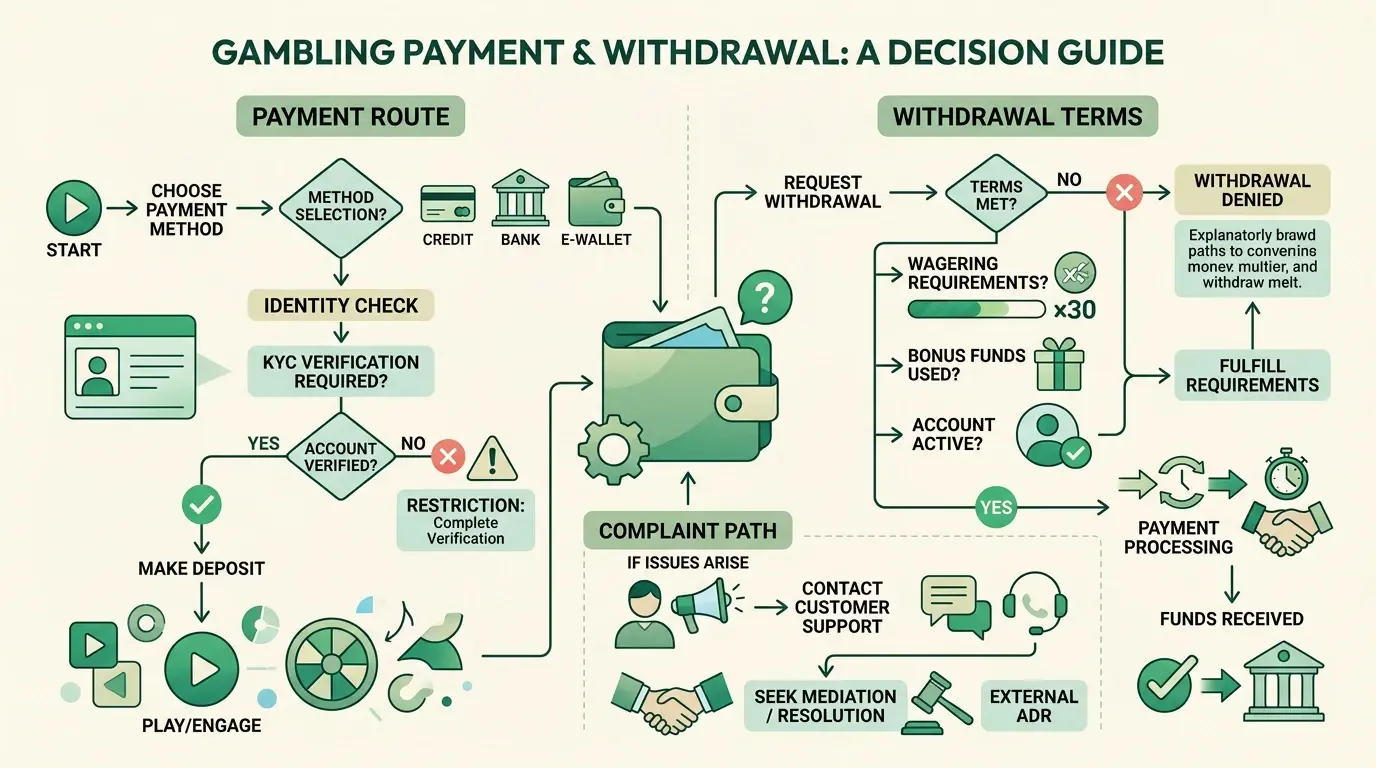

Before depositing: checks that do not rely on brand promises

The strongest commercial question is not “which site is best?” It is “what can I verify before I send money or documents?” That wording matters because it keeps the focus on checks you can perform without trusting a promotional claim. It also avoids the trap of turning a sensitive gambling topic into a list of supposedly safe shortcuts.

Start with the official Gambling Commission public register when the site claims a Great Britain licence or when the site presents itself in a way that should be checked against a GB-licensed activity. The public register can show licensed businesses, individuals, regulatory actions and premises. A useful check compares the business name, trading name, domain and licensed activities rather than stopping at a logo or a licence number copied into a footer.

If those details do not line up, pause. Do not fix the problem in your head by assuming the site is covered under another brand, a sister company or a payment processor. A domain mismatch, vague ownership statement or unclear restrictions can become important later if there is a dispute. The point is not to become a lawyer. The point is to avoid paying first and asking basic accountability questions after something goes wrong.

Pre-deposit checklist

Check the operator identity. Look for a real business or trading name and compare it with an official register when a licence is claimed.

Check the exact domain. A licensed business name does not automatically cover every website using similar wording.

Check restrictions and activities. A licence or permission can have limits. Do not assume every product, country or payment route is covered.

Check money terms. Read deposit rules, withdrawal conditions, bonus restrictions, customer-fund disclosure and the complaints process before paying.

Check your own boundary. If a self-exclusion, bank block or blocking tool is active, treat that as a reason to stop and review support options.

Customer funds are another area where casual wording can mislead. A gambling business may have to disclose whether customer money is protected if the business goes bust, and the level of protection matters. That is not the same as saying your money is always fully safe. The honest question is: what protection level is stated, where is it explained, and would you still deposit if the answer is unclear?

Complaints are similar. For licensed-operator contexts, the complaint process should point to a path for unresolved disputes, and alternative dispute resolution may become relevant where an operator cannot resolve a complaint within eight weeks. This does not guarantee an outcome. It does give you an accountability signal to look for before you are in the middle of a delayed withdrawal, account closure or document dispute.

Useful checking is slow and slightly boring. That is exactly why it works. A flashy page can make an immediate deposit feel like the natural next step. A structured check reverses that pressure: first prove who the operator is, then understand the money rules, then decide whether gambling fits your situation at all.

What counts as a warning sign?

A warning sign is not always proof of wrongdoing. It is a reason to stop, verify and avoid sending more money or documents until the situation is clear. Some warning signs relate to the operator; others relate to your own behaviour. Both matter.

More reassuring signs

Operator details can be matched to an official register when a relevant licence is claimed.

The exact domain, trading name and licensed activity are clear.

Terms explain deposits, withdrawals, bonus restrictions and identity checks in normal language.

The customer-fund statement and complaint route are easy to find.

Payment and control information does not encourage you to ignore a block or exclusion.

Reasons to stop

The site treats absence from GAMSTOP as if it proves trust or suitability.

Ownership, licence details or domain coverage are hard to verify.

Bonus terms are scattered, vague or different from the promotional headline.

Withdrawal rules appear only after a deposit or after a document request.

You are trying to gamble while a self-exclusion or bank block is active.

Check the operator and the money rules before the deposit, not after a dispute starts.

Payments, identity checks and withdrawals

Payment friction is not always a technical error. In Great Britain, credit-card gambling payments are banned, and that restriction also extends to e-wallet use of credit-card funds for gambling. Gambling companies cannot accept payments from e-wallets that do not block use of credit-card funds for gambling. If a payment route appears to work around that boundary, that is not a clever feature. It is a reason to slow down and check the official position.

Bank gambling blocks are different from operator terms. Many banks allow customers to enable gambling blocks through mobile banking or card controls, and the block may apply at card level. The useful way to view a bank block is as a protective layer, not as a fault to defeat. If you set the block yourself, or if someone you trust helped you set it up, treat the urge to remove it as part of the decision, not as a separate inconvenience.

Identity checks also deserve calm treatment. Online gambling businesses must verify age and identity before gambling. Document requests may include a passport, driving licence or household bill, although exact requirements and timing vary. A document request is not automatically suspicious, but it still raises practical questions: who is asking, under which operator name, for what purpose, through what secure process, and how will the information be handled?

Withdrawals and bonuses are where many misunderstandings begin. For licensed operators, deposit balance withdrawal rights and bonus/deposit separation are subject to regulator and consumer-protection expectations. Promotion conditions such as eligibility, deposit requirements, wagering requirements and withdrawal restrictions should be clear and easy to find. You should not have to reverse-engineer the basic cost of accepting a promotion after your funds are already locked into play.

A simple decision path before paying

Do I know who runs the site? If not, stop.

Can I match the domain and activity to a relevant official record when a licence is claimed? If not, stop.

Do I understand the payment route and any restrictions that apply to me? If not, stop.

Can I withdraw my own deposit balance without unclear bonus barriers? If the answer is buried or conditional, stop.

Am I trying to get around a protection I already put in place? If yes, move to support before any gambling decision.

The best time to understand verification, withdrawals and bonus rules is before the first payment. After a deposit, your attention can shift from “is this a good decision?” to “how do I recover what I already put in?” That pressure can make unclear terms feel acceptable. Reading first protects you from that pressure.

Complaints, customer funds and personal data

Accountability becomes most important when something goes wrong: a withdrawal is delayed, an account is closed, documents are rejected, or a complaint goes unanswered. A good check before depositing asks what route exists if that happens. If there is no clear complaints process, no independent route where one should exist, or no understandable explanation of how customer funds are protected, you are being asked to take extra risk before you have basic answers.

Customer-fund wording should be read carefully. A disclosure that money is protected at one level is not the same as a promise that every balance is risk-free in every situation. The practical question is whether the site explains the level clearly enough for an ordinary user to understand the risk. If the statement is missing or hidden, that absence is information in itself.

Personal data questions also need a realistic answer. You may be able to ask for data deletion in some circumstances, but deletion is not automatic in every circumstance. Gambling businesses can have legal, regulatory or dispute-related reasons to keep certain records. That does not mean you have no rights. It means you should not rely on a casual promise that your documents or account information can always be erased immediately on request.

Age assurance and identity-related processing should be proportionate and follow data-protection principles. In plain terms, a site should not be casual with identity documents, and you should not be casual about sending them. If you cannot tell who is receiving the documents, how the request connects to an account rule, or how the data is protected, pause before sending more.

Worked scenario: delayed withdrawal

Imagine a withdrawal is delayed and the operator asks for new documents. The useful response is not to keep depositing while hoping the delay clears. First, read the withdrawal and verification terms. Second, confirm the operator identity and domain. Third, look for the complaints process and the route for unresolved disputes. Fourth, keep copies of your own messages and uploaded-document confirmations. Fifth, avoid chasing losses while waiting for an answer. The goal is to reduce risk, not to turn the dispute into another reason to gamble.

Money questions should move in order: payment route, account checks, withdrawal rules, complaint path and personal control.

When support should come before comparison

If you are reading this while self-excluded, blocked by your bank, using blocking software, hiding gambling from someone close to you, borrowing to gamble or trying to win back losses, the most useful answer is not a list of gambling sites. The useful answer is to pause and strengthen the protections around you.

GAMSTOP is a free tool that allows UK residents to exclude themselves from licensed gambling websites and apps. The verified guidance used here says users choose a minimum exclusion period and that the exclusion cannot be removed during that minimum period. It also says GAMSTOP will not contact users when the minimum period expires; if the user does not ask to remove it, the exclusion remains in place for seven further years after the minimum period. Those details are important because they show that self-exclusion is designed to create time and distance, not a temporary inconvenience to be negotiated away during a difficult moment.

Bank blocks and blocking software can add further layers. They are not perfect, and they are not a substitute for support from people or services, but they can reduce the number of moments where a sudden urge turns into an immediate payment. If a bank block or software block is frustrating you, name the frustration honestly: the tool may be doing exactly what it was set up to do.

A protective pause

If you feel pulled toward gambling during an exclusion or after setting a block, step away from the device before making any account or payment decision. Use the protection already in place, speak to someone you trust, and consider specialist support. A safer next action can be as simple as not opening another gambling site today.

Support language should not shame the reader. People often look for practical gambling information at moments that are already stressful. The point is to make the safer path easier to see. If your main reason for searching is that a previous boundary is stopping you, the guide’s advice is to respect that boundary and move toward help rather than around it.

Official checks worth bookmarking

You do not need a long list of brands to make better decisions. You need a short list of reliable places to check the claims that affect your money, account and personal information. These pages are useful because they come before any operator promise.

Licence and domain checks

Use the Gambling Commission public register to check licensed businesses, individuals, regulatory actions and premises where a Great Britain licence is relevant. Compare the exact domain and business name rather than relying on a badge.

The Gambling Commission’s public guidance explains checks to make before gambling, including licence status, terms, complaints and customer-fund information.

If a dispute arises, understand the complaint path and when alternative dispute resolution may become relevant. Do not keep depositing while a complaint is unresolved.

The ICO explains the right to ask for personal data deletion in some circumstances. Treat this as a rights question, not a guarantee that every record can vanish immediately.

When a protective tool is active, the next useful step may be support, not another gambling decision.

How to use the focused guides

This page is the broad overview. The focused guides go deeper into one decision at a time, so you are not forced to mix self-exclusion, licensing, payments, identity checks and dispute routes into one confusing pile. Use them according to the problem in front of you.

Choose the next guide

What “not on GAMSTOP” means in practice explains the boundary between GAMSTOP coverage, licensing and personal suitability.

Checks to make before sending money gives a step-by-step way to review operator identity, domain details, terms, customer-fund disclosure and complaints.

KYC, withdrawals and bonus terms helps you read identity requests and money conditions before they become a dispute.

Payments and bank controls explains credit-card restrictions, e-wallet boundaries and bank gambling blocks without encouraging workarounds.

Support tools if gambling is hard to control puts self-exclusion, bank blocks, blocking software and help options first.

Complaints, customer funds and data questions covers accountability when a dispute or personal-information concern has already appeared.

Common questions

Does “not on GAMSTOP” mean a site is safer?

No. The phrase only points to a boundary around the GAMSTOP scheme. It is not proof that a gambling site is licensed, fair, accountable or suitable for you. A separate check of the operator, domain, terms, payment route and complaints process still matters.

Can a GAMSTOP exclusion be removed early?

The verified guidance used for this guide says the minimum exclusion period cannot be removed during that period. Treat that as a protection boundary, not a technical problem to work around.

What should I check before sending documents or money?

Check the official public register, the exact domain, the business or trading name, the licence activity, restrictions, terms, withdrawal rules, complaint route, customer-fund statement and privacy information. If those items are missing or confusing, stop before adding more money or personal data.

Are credit card gambling payments allowed in Great Britain?

The verified rule used here is that credit-card gambling payments are banned in Great Britain, and the restriction also covers e-wallet use of credit-card funds for gambling. A site or payment route that seems to ignore this should make you slow down and check official information.

Where does support fit if I am already self-excluded?

Support fits before any site comparison. GAMSTOP, bank gambling blocks, blocking software and direct support can work together as protective layers. Looking for a way around an active boundary can be a sign that it is time to pause and get help.

Final practical reminder

A careful gambling decision is not made by a slogan. It is made by checking who runs the site, whether the domain and activity match a relevant official record, how payments and identity checks work, what the terms say about your own money, what complaint route exists, how your data is handled and whether you are trying to cross a boundary that was meant to protect you.

If you cannot answer those questions calmly, the safest next step is to stop before depositing. If you are trying to gamble during self-exclusion, through a bank block or while chasing losses, the better next step is support. The point of this guide is not to make gambling look easy. It is to make the risk visible enough that you can decide slowly, clearly and with your own protection at the centre.